Tactical Positioning

Staying invested paid off in July as there was a significant rebound in markets and particularly in growth related sectors such as technology. For the time being, markets have moved up from the oversold position they had reached in June, but we have July inflation data looming on 10th August and this could dent investor enthusiasm if the numbers are too ‘hot’. Short term, we are not adding to equity exposure but we think there is a good chance, using an American term, that the ‘bottom is in’. That said, this is based on the US Federal Reserve moving to a less aggressive stance on interest rates by the last quarter of 2022.

Market Moves

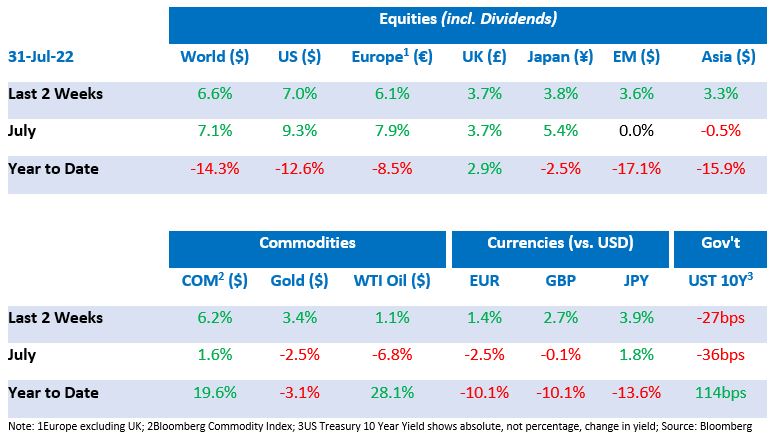

Financial Markets were strong in July

Equity and Bond prices rose strongly in July, taking the 10-year US Government bond yield 0.36% lower to 2.66% and global equities up 7.1% in US $ terms. A key reason for the increase is a growing expectation that inflation has peaked.

Will ‘interest rates up’ mean ‘inflation down’?

Central banks are trying to tame inflation by ‘tightening’ policy to squeeze demand. Although rates have been increased in most major markets, interest rates remain in negative territory in real terms (the interest rate minus inflation). Indeed, the gap between the inflation rate and interest rates has increased over the last eighteen months so it could be argued that policy is looser today than it was then.

The Federal Reserve (“Fed”) raised interest rates another 0.75% last week taking the Fed Funds Rate from a range of 0% to 0.25% in March to a range of 2.25%-2.5% today. Chair Jerome Powell stated that there will be a point when the Fed starts to slow its rate hikes to give time to assess their impact. US Treasury bond prices are consistent with the view that the US is either in a recession or likely to enter one shortly and that consequently the Fed will have to stop raising rates soon. Market pricing points to rates being raised to 3.25% in December this year followed by no hikes in 2023. The Fed’s other job of achieving full employment is faring better than their inflation target, with the unemployment rate holding at 3.6% in June.

In Europe, the European Central Bank (ECB) had led us to expect a 0.25% rate rise at the most recent meeting. The actual 0.5% increase seemed more appropriate given the 8.6% inflation number. To our minds it was right that the ECB did not feel compelled to follow their own guidance. This first hike in a decade came alongside the resignation of Italian Prime Minister, Mario Draghi, which could test the ECB’s anti fragmentation tool. Europe’s peripheral government bond yields have widened significantly with Italy’s at a concerning level.

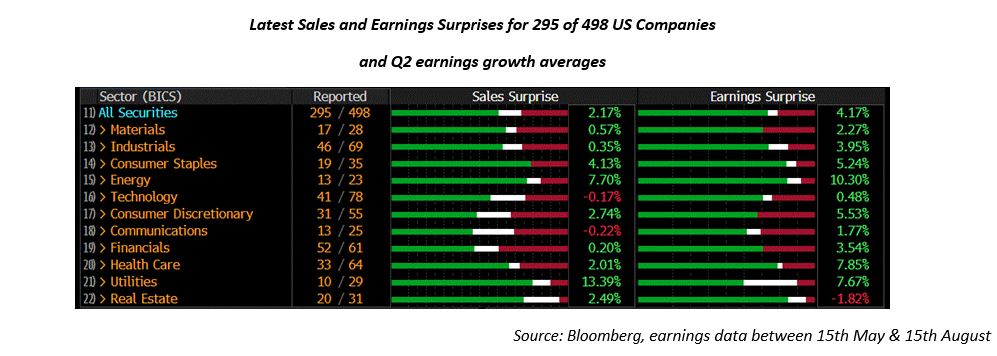

Company profits increasing whilst GDP falls

US GDP fell by 1.6% in the first quarter of the year and 0.9% in the second. Meanwhile company profits have continued to increase following last year’s strong rise of almost 50% in the US. Recent corporate earnings releases for the second quarter have tended to beat forecasts with profits from US companies currently on track to increase by over 8% this year. The fall in commodity prices (except gas) which reflects slower economic growth has also been taken as a positive signal that inflation may be about to wane.

Economic Updates

Data across the board has been mixed. The number of Americans filing new claims for unemployment were higher than expected for each of the last two weeks, but new home sales, and consumer confidence both disappointed. In the UK unemployment remained at 3.8% whilst inflation (CPI) rose 0.3% to 9.4%, just ahead of forecasts. Retail sales were down 5.8% compared to the previous year. European and German PMIs mostly came in below 50, which is an indicator of economic contraction, and this was the same for Chinese manufacturing indices.

In the first week of August market participants will be waiting for the US July payrolls number. The resilience of the employment market has been an important indicator of the real status of the US economy and with interest rates going up it will be interesting to see whether a weakening economy is reflected in the numbers. Other releases include the ISM index, trade balance and consumer credit alongside manufacturing-focused data that will be released in Europe. There are no Fed meetings in August, so it may provide time for markets to reflect, and re-ground themselves.

Download the bulletin here.