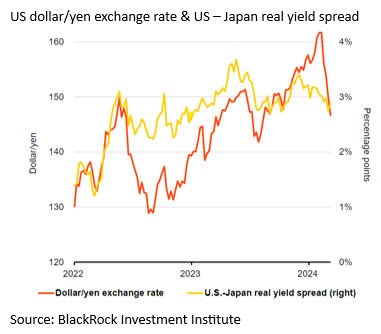

Tactical Positioning

We wrote at the end of July that that the prospect of imminent interest rate cuts would lend support to equity and bond markets, despite short term gyrations. As a consequence, for clients with relatively high levels of cash, we used recent weakness as an opportunity to top-up equity exposure. Despite geo-political worries, tantrums about recession and higher near-term market volatility the appetite for equities remains relatively strong and is now being driven forward by a robust wave of Mergers and Acquisitions and stock market IPOs (Initial Public Offerings) activity. US corporate earnings should show double-digit growth this year and the outlook for 2025 is also positive as the cheaper cost of borrowing drops to the bottom line.

Market Moves

Japan: The comeback kid

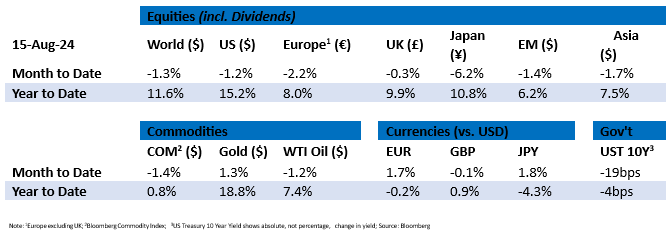

Following the Bank of Japan’s (BoJ’s) sudden rate hike in July coupled with plans to taper its bond purchases as well as their sudden willingness to incorporate the yen as a factor in setting policy, investors were quick to unwind their carry trades that were effectively borrowing in low-interest rate yen to buy other assets. The scramble to close these positions led to one of the largest unwinds in yen futures. The exact volume is difficult to quantify however, the chart below highlights the closing of the gap between Japanese yen and US dollar yields (yellow line) and the sharp rise in the value of the yen (the red line falling).

This led to Japan’s stock market experiencing the most severe one-day sell-off since 1987 (of 12%), as well as its worst three-day stretch ever. The market volatility was somewhat placated by comments from BoJ Deputy governor Shinichi Uchida who said interest rates would not be raised whilst markets are unstable. By the end of the week, markets had regained most of the lost ground with Japan’s broader index down only 2.1%. Given these dramatic price swings, it is likely that the BoJ will proceed cautiously to avoid another sharp spike in the yen and the chances of a rate hike in October has fallen further given the announcement of Prime Miniter Kishida’s decision to resign.

The stock market’s rollercoaster ride

The volatility in Japan reverberated across global markets and as the US unemployment rate ticked up to 4.3% it was spurred on by fears that the US Federal Reserve (the Fed) has fallen behind the curve on rate cuts and will not be able to execute a “soft landing”. The major global equity indices plummeted and US equities neared correction territory when the main index fell 9.7% from its mid-July high while the US technology index was also down 15.8% from its peak.

Despite this, fears of an economic crisis appeared overstated as markets recovered from the sell-off and generally ended the two-week period only modestly lower. While data remains mixed, a strong Institute of Supply Management reading showed the services sector rebounding from contraction to expansion territory, and investors still expect US corporate earnings to deliver double digit growth. This suggests that consumer and corporate spending is moderating but looks durable.

Is inflation no longer the biggest concern?

The US CPI data release on Wednesday saw inflation fall, for a fourth straight month, to below 3% for the first time since 2021. This highlights that inflation is trending slowly in the right direction, which is good given that it seems consistent with a soft-landing and supports the case for the interest rate cuts that have already been priced in by markets. However, The Fed Bank of Chicago President, Austan Goolsbee, has stated he is growing more concerned about the labour-market than inflation given the backdrop of the poor jobs data and price pressures. Additionally, he stated that current interest rates are “very restrictive”, saying they would only be appropriate if the economy were overheating. The balance between inflation and labour-market risks poses an interesting backdrop to the Fed’s September meeting with Fed Chair Jerome Powell also highlighting their focus on preventing a downturn in the jobs market.

Economic Updates

As stated, the weaker-than-expected unemployment rate for July led investors to believe that the Fed was falling behind in its response to weakening economic conditions. However, the weekly jobless claims data eased concerns as it fell over the fortnight, first by 17,000 to 230,00 and again in the following week to 227,000. Adding to the resilience of the US market was a strong retail sales data release that came in well above the expected 0.4% at 1.0% for the month.

The monthly Consumer Price Index (“CPI”) reading came in as expected at 0.2% taking the year-on-year CPI to 2.9%. This supports the notion that inflation is still broadly on a downward trend and the Fed is likely to lower interest rates.

In the UK, year-on-year CPI increased 2.2% in July versus the expected 2.3% moving back above the Bank of England’s (BoE) 2.0% target. The Office for National Statistics has attributed the increase to housing and household services. Preliminary GDP releases have come in as expected with growth over the quarter at 0.6% indicating the UK economy continues its recovery from recession.

In China, inflation rose faster than expected in July, with CPI reaching a five-month high of 0.5% year-on-year, compared with 0.2% in June and surpassing markets forecasts of 0.3%. Extreme weather causing disruptions to supplies partly drove this increase. However, these supply side factors are unlikely to remain.

Download the bulletin here.