Tactical Positioning

We mentioned in our last bulletin that market ‘tantrums’ relating to fears of a sharp slowdown in the US economy looked like decent buying opportunities. The first two weeks of September seem to have confirmed this with a sharp sell-off in the first week and a corresponding rally last week. During the past nine monetary easing cycles in the US, the main US equity index rose when the economy was still growing. Whilst growth could be shallower over the next 12 months, we think a recession is highly unlikely. With this in mind, we continue to ‘buy the dips’ for those building their equity exposure.

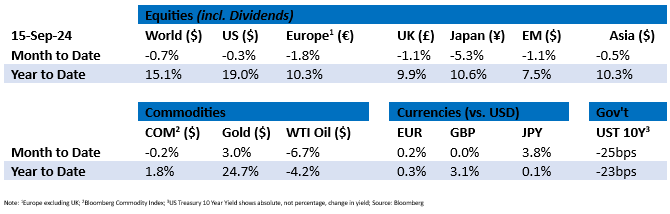

Market Moves

Harris-Trump showdown

The first presidential debate between Vice President Kamala Harris and former President Donald Trump took place on Tuesday 10th September and was viewed by an impressive 67 million people. The pair argued their cases on issues including the US economy, immigration, inflation, and tariffs. Perhaps unsurprisingly, Trump and his supporters accused ABC TV of bias. Post-debate, Trump was challenged to a second head-to-head in October, but he announced that he has no intention of another face-off. According to the two-day Reuters/Ipsos survey which closed on Thursday, Harris extended her lead in the presidential race to 47% of the vote versus 42% for Trump following the showdown, although other polls show a more even race.

The overall impact of the debate on financial markets remains uncertain. Wednesday saw the decline of a number of stocks within the ‘Trump trade’ category, including cryptocurrency related investments and the former president’s Trump Media & Technology Group which owns Truth Social, falling by close to 15% over the course of the day but recovering almost all of its losses by the end of the week. On the other hand, stocks related to the green economy and renewable energy benefitted from what is believed to be a Harris win while healthcare stocks fell during the immediate aftermath of the debate.

All eyes on the Fed

The next Federal Open Market Committee (“FOMC”) monetary policy meeting takes place this week and market participants are divided on whether to expect a 25 or 50 basis point rate cut. The FOMC has maintained the federal funds rate at 5.25%-5.50% since July 2023, following a series of rate hikes aimed at curbing high inflation. While the recent move in the futures markets and concerns about a rapidly slowing economy had pointed to a more aggressive move by the Federal Reserve (“Fed”), the latest US jobs numbers were not as weak as feared and last week’s month-on-month core CPI data came out slightly higher than expected at 0.3% compared to the forecast 0.2%. By the end of last week, there was an equal chance of either scenario according to CME’s FedWatch tool. However, sentiment shifted quickly over the weekend and markets are now in favour of a more aggressive stance by the Fed with a 61% probability of a 50 basis points cut versus 39% for a 25 basis points cut. US equities have rallied as investors await the Fed’s decision, with the main index producing its best weekly performance of 2024 last week, increasing by around 3.5%.

Gold rush

Gold prices reached a new all-time high of around $2,589 per ounce, producing a year-to-date return of close to 25%. The price of the precious metal has been supported by geopolitical tensions, a weaker US dollar and the fall in global interest rates.

Global inflation watch

There was a plethora of Consumer Price Index (“CPI”) releases over the fortnight. Swiss inflation was unchanged in August, sitting at an annual rate of 1.1%, below the 1.2% expected, whilst annual inflation in China increased to 0.6% in August, up from 0.5% in July and below market forecasts of 0.7%. In the US, annual CPI inflation cooled to 2.5%, down from 2.9% in July. US core CPI rose slightly more than expected in August, at 0.3% on a monthly basis versus 0.2% expected. Producer prices in the US also eased to 1.7% from 2.1% and below the expected 1.8%.

Economic Updates

The Bank of Canada cut its policy rate by 25 basis points to 4.25% and the European Central Bank cut interest rates for the second time this year, reducing its deposit rate by 25 basis points to 3.50%. The moves by both banks were in line with expectations.

In the US, the economy added 142,000 jobs in August, behind the projected figure of 164,000. The headline unemployment rate also edged down to 4.2% from 4.3%. In Canada, employment was little changed in August with 22,000 jobs added and an increase in the unemployment rate to 6.6% from 6.4%.

In the UK, unemployment fell 0.1% to 4.1% in the three months to July. Monthly real gross domestic product (“GDP”) was unchanged in July, making the month the seventh consecutive month in which GDP has not fallen. On a rolling quarterly basis, GDP rose 0.5% in the three months to July, below April to June’s expansion of 0.6%.

Download the bulletin here.