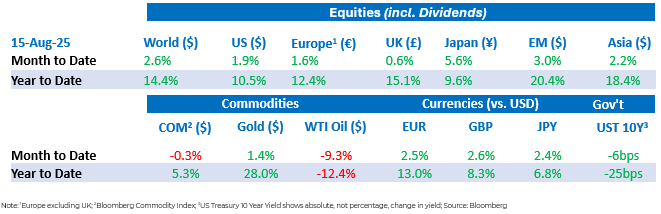

Tactical Positioning

Over the past fortnight US equities extended their rally with major indices logging their third winning week in four and most reaching new all-time highs. The momentum has been fuelled primarily by strong tech sector earnings — notably from mega-cap names such as Nvidia and Apple — as well as broadly positive corporate results in sectors like healthcare and travel. This earnings-driven optimism has helped offset short-term concerns about tariffs and monetary policy uncertainty. However, sentiment among institutional investors is turning cautious. According to the latest Bank of America Securities Global Fund Manager Survey, a record 91% of respondents now believe that US equities are overvalued, the highest reading since the survey began. This growing perception of stretched valuations could leave the market vulnerable to short term profit-taking, particularly if macro data surprises negatively or if policy rhetoric shifts more hawkish.

Market Moves

Central bank policy and data credibility

A surprise resignation at the US Federal Reserve (“Fed”) has opened the door for President Trump to nominate a replacement, with Stephen Miran — known for his preference toward looser monetary policy — emerging as a potential candidate. Markets are now factoring in the possibility of a more accommodative Fed stance with a quarter point cut in rates expected at the September policy meeting, though no official shift has been signalled. In Europe, the European Central Bank’s (“ECB”) hawkish tone has been reinforced by July’s stronger-than-expected inflation data, suggesting rate cuts remain unlikely in the near term. Meanwhile, concerns are growing over the politicisation of economic statistics in the US, as changes at key data agencies raise questions about the independence and credibility of official figures. This mix of policy uncertainty and institutional trust issues is adding a layer of complexity to global market sentiment.

Trade tensions

The US–China trade tensions saw a temporary easing as President Trump extended the tariff truce with Beijing by 90 days, avoiding an immediate escalation between the world’s two largest economies. However, Washington simultaneously moved to broaden its protectionist stance, raising tariffs on more than 90 countries effective at the start of August. The measures included sharp increases such as 50% on Indian goods, up to 145% on Chinese imports if no deal is reached, 35% on Canadian exports, 25% on Mexican goods, and 15% on products from the EU and Japan. While the EU successfully negotiated to keep its tariffs capped at 15%, the overall shift reignited fears of slower global trade flows. Markets reacted negatively to the tariff news with European equities in particular facing pressure amid concerns over supply chain disruptions and higher input costs, but remain supported by continued evidence of strong corporate earnings growth.

Latin American currencies and commodities

Latin American currencies have continued to outperform global peers, supported by high local interest rates, strong carry trade inflows, and relatively stable domestic economic conditions. The Brazilian real and Mexican peso have been the main beneficiaries, helping push the LatAm FX index, which measures the performance of the currencies of Mexico, Brazil, Colombia, Chile and Mexico against the US dollar, to gains of over 20% year-to-date. Much of the increase reflects the weakness of the dollar which is down 13% against the euro this year). Analysts caution, however, that the rally may face headwinds if US bond yields rise further or if commodity prices soften, reducing export revenues. In commodities, gold prices, which are up 28% in dollar terms this year, rose over the fortnight but by less than the amount the dollar fell. Oil prices fell by 9.3% over the fortnight but remains within recent trading ranges as supply-side constraints balance concerns over slower global demand from tariff disputes. On the investment side, India has emerged as a hotspot for real asset inflows, particularly in real estate and infrastructure, attracting significant foreign capital owing to strong economic growth and favourable policy frameworks. This trend reflects a broader global search for tangible assets that can provide both yield and inflation protection in an uncertain macro environment

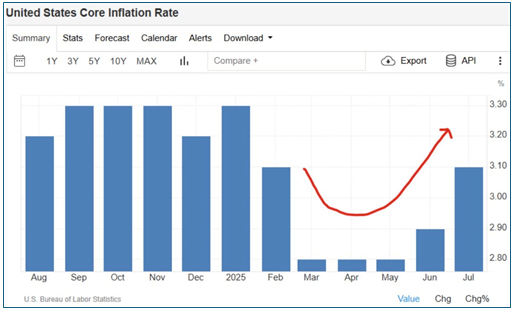

Inflation ups and downs

US inflation as measured by the consumer price index held steady in July, at 2.7% slightly below market expectations and consequently increased the probability of a rate cut in September. However, core inflation, as shown in the table below, rose to 3.1% up from 2.9% in June and 2.8% in the three prior months.

Two days after the announcement of the consumer prices index (“CPI”), the US Producer Price Index (“PPI”) surprised sharply to the upside. Headline PPI rose 0.9% month-on-month (3.3% year-on-year) versus expectations of 0.2% and 2.5%, marking the strongest monthly increase since March 2022. Core PPI also climbed to 3.7% year-on-year, reflecting ongoing service-sector price pressures already visible in consumer indices and reinforcing the signal of underlying price pressures. The hotter-than-expected PPI data has reduced expectations for aggressive Federal Reserve rate cuts. The 2-year Treasury rose to 3.72% and the 10-year to 4.26% following the announcement while equity markets softened as investors recalibrated expectations.

Economic Updates

The US labor market continues to be resilient, with the unemployment rate currently just 4.2% and job openings running slightly above the number of unemployed. Globally, the IMF upgraded its growth forecast, projecting 3.0% in 2025 and 3.1% in 2026, citing pockets of resilience across advanced and emerging markets. However, trade tensions, geopolitical risks, and elevated inflation continue to pose downside risks. In Europe, inflationary pressures intensified, with July Eurozone CPI reaching 2.5% year-on-year and core inflation also rising, reinforcing expectations that the ECB will maintain a restrictive monetary stance in the near term.

Download the bulletin here.