Tactical Positioning

Market volatility remains high, as investors worry about how far central banks will raise interest rates in response to inflation. Although we are optimistic that the end of covid restrictions will be good for economic growth, we see growing risk that if interest rates rise too rapidly this may trigger an economic slowdown. In the short term there is the additional risk that a war in Ukraine could lead to further increases in oil and gas prices which in turn could push headline inflation higher whilst reducing demand for other goods and services, as a larger share of company and consumer expenditure is directed towards energy costs. Within portfolios we maintain exposure to quality growth equities, which should be less vulnerable to the economic cycle, whilst having exposure to sectors such as banks, which are beneficiaries of higher interest rates.

Market Moves

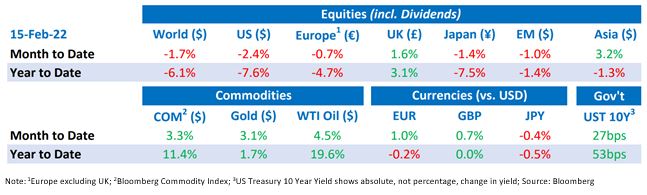

Equity markets generally fell over the fortnight, although the UK equity market which is dominated by banks and resource companies was a beneficiary of higher oil prices and interest rate expectations.

Inflation – Is it just transitory?

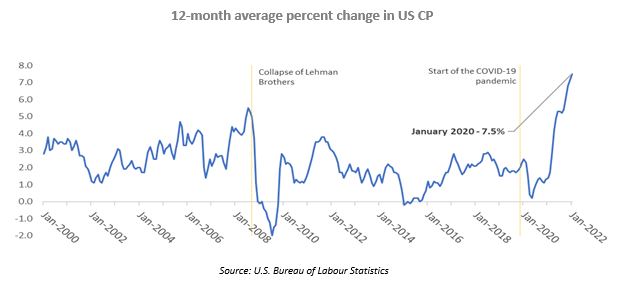

The headline news of the fortnight was the release of the January Consumer Price Index (“CPI”) figures from the US Bureau of Labour Statistics. The 7.5% annual increase, which managed to exceed consensus estimates of 7.3%, is the largest increase in consumer goods prices for 40 years. The primary contributors to the large inflation figure were energy, namely gasoline, and used vehicles, owing to the ongoing semiconductor supply chain bottleneck impacting the production of new cars. Those remaining in the transitory camp argue that these supply pressures, which drove the surge in inflation over 2021/22, are already reducing. Others argue that the shift to sustainable assets and net-zero targets will continue to drive inflationary pressures for years.

Interest rates on the increase

Following the January CPI release in the US, investors have been bracing themselves for how aggressively the Federal Reserve (“Fed”) will act to try to curb inflationary pressures. Markets have already priced in a 50 basis point rate increase in March, with St Louis Federal Reserve Bank President James Bullard stating his support for a full percentage point rise in rates over the next few Fed policy meetings. Poised for further rate hikes, the yield on the US 10-year Treasury bond rose 27 basis points month-to-date to reach 2.00% for the first time since August 2019. This is three times the low level they reached early in the pandemic. Although interest rates are set to rise, we believe that they will settle at a relatively low peak and are likely to be below average inflation levels for the next couple of years. This will leave real, inflation adjusted, interest rates at historical lows and should support the price of risk assets.

Still time for diplomacy

As tensions continue to rise at the Russo-Ukrainian border, with Russian troops deployed en-masse to conduct “combat training exercises”, US President Joe Biden and British Prime Minister Boris Johnson insist that there is still time for a diplomatic conclusion to the affair. At the same time, both nations continue to advise their citizens to leave Ukraine whilst they can, by any commercial means available. German Chancellor Olaf Scholz visited Ukraine at the start of the week and then travelled to Moscow shortly after, following in the footsteps of French President Emmanuel Macron. Russia’s Defence Ministry announced on the morning of the 15th that “some troops will be returning to their bases from the Ukrainian border after completing drills”. Even though the announcement has not been formally verified by satellite imagery, the release in pressure was enough to prompt a snap rally in markets, with US equity futures rising as much as 1.80%, amid hopes for continually reduced geopolitical tensions.

‘You’ve got a friend in me’

Russia’s emerging ally, China, supported the anti-NATO rhetoric, claiming that “Western powers are using the NATO defence alliance to undermine Russia”. Relations between Russia and China appear to have bloomed into a renaissance in 2022, with China lifting restrictions on Russian wheat and barley imports and Vladimir Putin attending as the guest of honour at the opening ceremony of the Beijing Winter Olympics. An announcement that state-owned energy company Gazprom will sell an additional 10 billion cubic metres of gas to the China National Petroleum Corporation, as part of a 30-year agreement worth approximately US$118 billion helped to solidify relations between the global superpowers.

A light at the end of the tunnel…

Covid restrictions continue to ease. In the UK, for example, Boris Johnson announced that he is considering ending all COVID related restrictions, including the self-isolation requirement, by the end of February, one-month earlier than his previously stated date. He pointed to the continually dropping case numbers and hospitalisations as well as the antibody wall developed by fully vaccinating over 65% of the eligible population.

Economic Updates

The University of Michigan’s Consumer Sentiment Index reached its lowest level in a decade, falling from 67.2 to 61.7 for February, driven by an inflation-linked weakening in personal financial prospects and lower confidence in the US government’s economic policies.

Download the bulletin here.