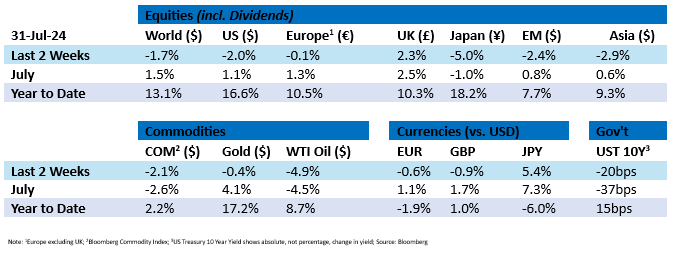

Tactical Positioning

In our last bulletin we wrote that we continued to expect the rally in markets to pause in the coming weeks and that jitters might lead to profit taking. To some extent, the market gyrations of the last two weeks seem to have borne this out. Whilst more volatile conditions could persist during August and early September, we believe that downside risk is limited by the imminent arrival of US rate cuts. At the end of June, investors were only expecting a single rate cut in 2025 but weakening macro data in the last month has led to a gradual change in view with 2 or 3 rate cuts now expected by the year end. We believe these expected rate cuts will ultimately underpin markets and the case for a full weighting in equites and bonds remains intact.

Market Moves

A summer storm in the US

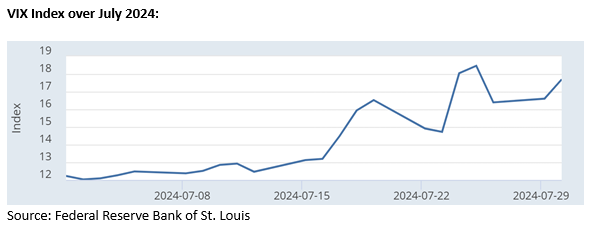

The US equity market has seen volatility increase recently. The VIX (volatility index), often referred to as the “fear gauge,” has risen over 30% in July, highlighting a shift towards a risk-off approach as investors grapple with uncertainties surrounding the upcoming election, the nuances of the Artificial Intelligence revolution and what might follow the dominance of the “Magnificent 7”. In recent weeks, there has been a rotation away from growth stocks, particularly in the technology sector, perhaps indicating profit-taking and a broadening of market leadership. NVIDIA, the standout performer of the year, has tested shareholders’ nerves, falling over 17% during the month before rebounding nearly 13% on 31st July. Investors, betting on a September rate cut, also started buying small cap stocks again.

Investors’ perception of potential risks appears to be changing. According to Bank of America’s monthly fund manager survey, the most significant tail risk is now geopolitics, which has overtaken concerns about inflation and high interest rates. Large multinational growth companies with global supply chains are particularly vulnerable to geopolitical instability. A recent example is the 10% drop in ASML’s stock price over the past month, driven by investor concerns following reports that the US may consider tougher restrictions on semiconductor equipment sales to China, citing national security risks.

The land of the rising rates

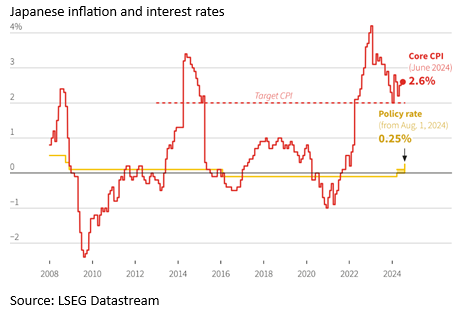

The Japanese yen hit a four-month high against the dollar last week after the Bank of Japan increased its benchmark interest rate from 0.1% to 0.25%, marking the largest hike since February 2007. Additionally, the central bank announced plans to halve its monthly bond-buying programme to 3 trillion yen by Q1 2026, reflecting Governor Ueda’s commitment to a normalisation of monetary policy. Japanese equities fell on concerns that a strengthening yen could dampen exports and that higher rates may weigh on the real estate sector and companies with debt. Interest rates in Japan are moving in the opposite direction to most major central banks and further cuts in the coming months could fuel the yen to strengthen further.

High stakes and air strikes: Tensions soar in the Middle East

An Israeli airstrike in Beirut and the killing of a senior Hamas political leader Ismail Haniyeh in Tehran has further escalated tensions in the Middle East, raising concerns that the violence could spread and increase the risk of a full-blown war in the region. The situation has sparked fears of potential disruptions in oil supply routes, particularly through the Strait of Hormuz, a critical passage for global oil shipments. These concerns have led to a rise in the price of gold to an all-time high and a rebound in crude oil futures, which had recently hit a seven-week low, with the price of a barrel of brent oil rising to $80.65. Despite these geopolitical concerns, oil prices could remain pressured by weak demand from China, the world’s largest crude oil importer.

Economic Updates

In the US, the Conference Board consumer confidence indicator for July, which was announced on Tuesday, was slightly stronger than the previous month, but not enough to change perception that growth may be slowing nor sufficient to reduce expectations that the Federal Reserve will cut interest rates at their meeting in September.

Lower inflationary pressures continue to support interest rate cuts elsewhere too. In the UK, the Consumer Price Index (“CPI”) came in at 2.0% in June, which was marginally higher than expected but in line with the previous month. UK retail sales were down 1.2% which was weaker than expected. In Europe, the CPI flash estimate was 2.6% in July, 0.1% higher than expected as well as 0.1% higher than June.

Download the bulletin here.