Tactical Positioning

In our mid-May bulletin we wrote that ‘we remain positive on equities and shorter dated bonds but are reluctant to chase markets after such a solid recovery in a relatively short period’. We echo this guidance as we enter June with European and US equity markets sitting just a few percent below their all-time highs. Trade manoeuvres will dominate the short term direction of markets with policy confusion seemingly inevitable.

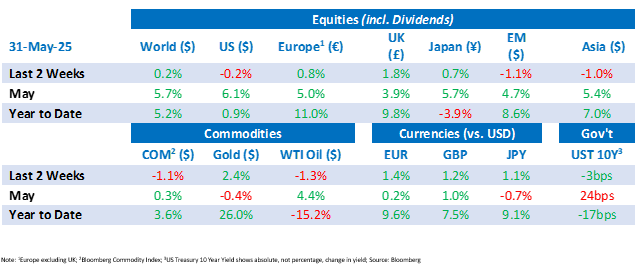

Market Moves

US debt downgraded…. again

The rating agency, Moody’s, finally matched S&P and Fitch by downgrading US sovereign debt. The reduction means the US has lost its last triple-A credit rating, after losing the first in 2011 and second in 2023. Their reasoning cited a lack of progress from numerous past Congresses and administrations to address rising fiscal deficits and federal debts. However, unlike 15 years ago when volatility spiked and equities pulled back, markets seemingly took the decision in their stride. This reaction was hardly a surprise as Moody’s has had the US on negative watch since November 2023 and major index providers had already moved US government debt to the double-A bucket. The US equity market closed slightly up on the day of the announcement while the 10 year Treasury yield was little changed.

Despite this, investors should not downplay the long-term fiscal challenges the US is facing. The move has shone a light on the worsening fiscal outlook at a time when Trump’s “Big Beautiful Bill” is in the process of being passed by Congress.

Trump vs EU

Investors were reminded that trade developments are still a key issue for markets when Trump introduced fresh tariff uncertainty by threatening to impose a 50% tariff on the European Union citing a lack of progress in negotiations. This led initially to European equities falling 2.4% on the news before the market rallied as investors seemed to bet that Trump’s threat was a negotiating tactic and the market closed the day only down 0.9%. Following a conversation with Ursula von der Leyen, the president of the European Commission, President Trump agreed to delay the tariffs until 9th July. Stocks rallied globally and most sectors of the US have gained since the announcement, led by growth-style sectors such as technology.

How the EU navigates the upcoming negotiations will likely impact markets. While it is unlikely that tariffs between the EU and US will rapidly spiral higher as the they did between the US and China, there remains the risk that the final conclusions damage growth or the inflation outlook. Both China and the EU have large goods trade surpluses with the US. However, the key difference is that the EU is mainly intra-industry trade, meaning the two economies trade largely in the same industries such as cars and pharmaceuticals. For now, the EU speaks of pursuing strategic patience, taking a softly-softly approach and using expansionary domestic policies to absorb the initial tariff impact.

Presidential overreach?

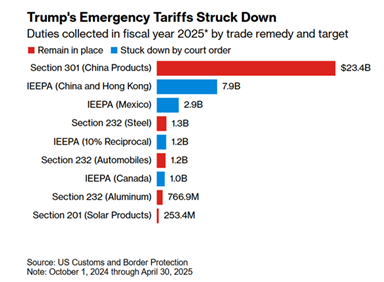

On Wednesday 28th, a ruling by the US Court of International Trade and a US District Court blocked President Trump’s tariffs stating he had exceeded his legal authority, had no right to “impose unbounded tariffs” and gave his administration 10 days to implement their orders. This would mean that the baseline 10% tariff, the reciprocal tariffs scheduled to take effect, and the 25% fentanyl tariffs would be void and already most are suspended.

The tariffs imposed under the 1977 International Emergency Economic Powers Act, claimed trade deficits created a national emergency were deemed illegitimate. This ruling did not however apply to tariffs on steel, aluminium and automobiles. Should the judgement remain, some estimate that it will create a $2 trillion hole in the US fiscal outlook over the next 10-years and remove duties that could have generated $200 billion annually.

The Trump administration immediately appealed both decisions and the US Court of Appeals granted a stay on the trade court ruling and we await a decision on the District Court ruling. This could potentially be escalated to the Supreme Court, a process that could take months. The effective US tariff rate is now 6.5%, down from the previous 15% assumption. The administration is likely to attempt to impose new tariffs under different legislation.

Given these and further trade tensions following Donald Trump’s claim that China has violated its tariff truce, it is hardly surprising that markets currently lack clear direction.

Are super-long JGBs in trouble?

Amid a pronounced weakening of supply/demand in the Japanese super-long-dated government bond market, several media outlets reported that Japan’s Ministry of Finance had sent a questionnaire to market participants asking their views on issuance. This prompted many to question the possibility of a reduction in super-long Japanese Government Bond (“JGB”) issuance. The speculation caused by these reports triggered a rally in prices and led to the country’s 30-year yield falling by more than 19bps in a single session, the biggest one-day decline since the regional banking turmoil in March 2023.

However, following a very weak 40-year auction this week, JGB yields have reversed some of their earlier rally. The 40-year yield rose 5bps following the sale. The continued decline in demand supports the narrative that the Japanese treasury will reduce its issuance of super-long bonds.

Economic Updates

In the US the Fed’s preferred inflation measure, Personal Consumption Expenditure (“PCE”), fell more than expected to 2.1% in April slightly below the anticipated 2.2%. Core PCE, which excludes more-volatile food and energy prices, dropped to 2.5% from 2.7%. Although PCE inflation is slowly approaching the Fed’s 2% target we expect the central bank to delay cutting rates at their next meeting as it gathers additional data to assess the impact of tariffs on inflation. This is supported by a healthy labour market where unemployment remains low at 4.2% and job openings roughly in line with unemployment.

In Europe business activity contracted in May as the service sector experienced a sharp deterioration. The Eurozone Composite Purchasing Managers Index fell to 49.5 from 50.4 in April. The European Commission reduced its late 2024 economic growth projection for the euro area in 2025 to 0.9% from 1.3%. This largely reflects the rising tariffs and trade policy uncertainty.

In the UK data was mixed. Inflation accelerated to 3.5% in April, boosted by higher utilities and housing prices. This is the highest level since January 2024. Contrastingly, retail sales rose 1.2% on the month which was well above expectations. Consumer confidence also ticked up from its low May levels.

Download the bulletin here.