Tactical Positioning

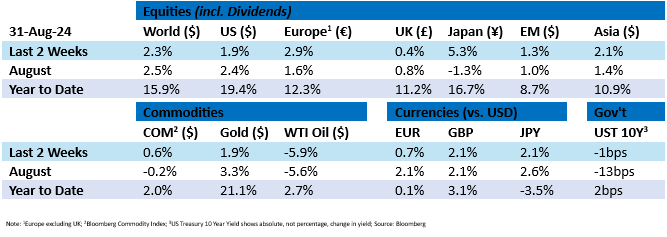

Market Moves

Cutting through the noise

Following Fed Chair Jerome Powell’s much awaited comments at the annual symposium in Jackson Hole, Wyoming on 22nd August, an interest rate reduction is expected in mid-September with the CME FedWatch Tool suggesting rate cuts of nearly 100 basis points by the end of the year. Powell claimed that “inflation is on a sustainable path back to [the Fed’s target of] 2%”, noting that inflation has fallen to 2.5% over the last year. He asserted that the labour market has cooled with the unemployment rate at 4.3%, a 1% increase on the early 2023 position and offered reassurance that the labour market will not cause inflationary pressure in the near term and that policy adjustments are due.

Following Powell’s comments, there was a positive shift in investor sentiment and US stocks approached record highs. Bond yields fell with the 10-year Treasury yield falling by 8 basis points reflecting the Fed’s more dovish position. To an extent, Powell’s comments were already priced into the market. However investors observed the notable omission of “gradual” in his announcement, potentially leaving scope for cuts larger than 0.25%.

Fuelling the fire

Following an escalation in hostilities between Israel and Hezbollah which resulted in the heaviest exchange of fire in recent months, tensions remain high although not yet reaching levels of total war.

Concerns about political instability in the region and elsewhere led to oil prices rising with Brent crude coming close to $82 per barrel. Supply concerns emerged as Ukraine focused attacks on Russia’s oil infrastructure and Libya closed its oilfields, halting production and exports. That said, supply has not been impacted drastically to date despite the ongoing fighting in Ukraine and the Middle East.

A million dollar gold bar

Another outcome of Powell’s speech was a further increase in the price of gold – you may be interested to read that with the price of gold above $2,500 the price of a bar of gold (weighing 400 troy ounces) is now above $1 million for the first time. The recent increase has been widely attributed to investors’ response to geopolitical risks, expected interest rate cuts and central bank buying. Unsurprisingly, since the US dollar and gold are negatively correlated, the US dollar hit its lowest level since July 2023 last week.

When great results are not enough

Nvidia published impressive financial results with record quarterly revenues of $30 billion, a 122% increase from this period last year and a 15% increase from the previous quarter. Despite these results, Nvidia’s shares fell 8% in extended trading after failing to surpass investors’ expectations.

Labour’s diplomatic deals and fiscal feel

Prime Minister Sir Keir Starmer made two diplomatic visits over the fortnight. First, a visit to Berlin during which a new treaty was discussed with German Chancellor, Olaf Scholz with a view to enhancing cooperation in several areas including trade and defence. It is hoped that this treaty will also address market access issues. Secondly, Starmer held talks with France’s President, Emmanuel Macron on similar issues. The UK’s fiscal outlook is looking less rosy. UK Chancellor, Rachel Reeves, issued a warning about the impending October budget mentioning “difficult decisions” relating to the alleged £22 billion deficit in public finances. Tax increases and public spending cuts seem like a foregone conclusion and Reeves did not rule out inheritance and capital gains tax increases in her 30th October Budget.

Kamala Harris’ first interview

In Kamala Harris’ first interview as presidential nominee, she emphasised her plans for the economy including the need for sustainable economic growth through investment in infrastructure, education and clean energy, and maintaining market stability. She defended the White House’s current track record under Joe Biden and stated there is more to do. She aims to “strengthen the middle class” and talked about her “opportunity economy” bringing down everyday costs and price gouging, investing in small businesses, extending child tax credit and prioritising affordable housing measures. She blamed the economic slump during the pandemic on Donald Trump’s mismanagement. Following the interview, two leading bookmakers noted that her popularity had declined. On Thursday, she was the favourite to win with 52.4% of the vote, however, on Friday, Trump’s chances of victory had improved from 48.8% to 51.2%. At the time of writing, there is no noticeable impact on markets following her comments as the content of the interview was as expected.

Freight frustrations

Canadian rail networks, CPKC and Canadian National shut down operations last week, causing potential supply chain disruptions in North America. This industrial action was the result of ongoing labour disputes that have lasted nearly a year. The stoppage lasted two days and culminated in government intervention forcing members to enter binding arbitration during which strikes are not permitted. Whilst this solution may only be temporary, the union involved plans to appeal to the federal court. Historically, strikes such as these have lasted up to nine days.

Economic Updates

In the US the Fed’s preferred inflation measure, core Personal Consumption Expenditures (“PCE”) price index, which excludes food and energy costs, remained stable in July with core PCE, at 2.6% year-on-year.

German CPI data released on Thursday fell to 1.9% year-on-year which was a decrease from July and the lowest inflation rate in more than three years. For the Eurozone, data released on Friday showed annual inflation had reduced to 2.2%. With lower inflation, the European Central Bank is very likely to cut rates (by 25 basis points) when they meet on 12th September.

Further afield, Japanese core CPI which excludes fresh food increased by 2.7% year-on-year which was a slight increase from the previous month making August the twenty-eighth consecutive month that core CPI has been above the Bank of Japan’s 2% target. These increases are driven by rising import prices, wage increases, government measures and economic recovery.

In response to Bank of England Governor, Andrew Bailey, taking a more cautious stance than Fed Chair Jerome Powell regarding interest rate cuts, sterling hit a two-year high against the US dollar, reaching $1.3246 at its peak, the highest since April 2022.

Download the bulletin here.