Tactical Positioning

We continue to be fully weighted in bonds and equities and maintain a bias towards growth stocks within the context of broadly diversified portfolios.

In terms of share price performance, the Magnificent 7 companies (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) stocks may take a ‘breather’ in the coming months, but there is continued excitement surrounding ‘growth’ stocks and their long-term upside potential. It is estimated that these 7 spent over $370bn on capital expenditure and research & development in 2023 including a significant amount on AI (artificial intelligence). The incredible levels of cash generated by this group currently dominate the US stock market and cannot be ignored and their earnings growth in 2024 is expected to be more than 20% with similar rates in future years and this is around 3 times the average for the rest of the market.

Market Moves

A divided world

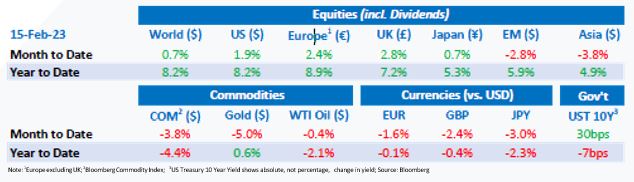

Equity markets in Europe, the US and Japan performed well over the fortnight on hopes that the economic environment will be strong enough to facilitate corporate profit growth whilst reduced inflationary pressures will lead to lower interest rates. Meanwhile in Asia, continued concerns about the economic outlook for China continue to weigh on markets.

In the week leading up to Valentine’s Day, investors continued devotion to US quality growth companies drove the US equity market to record levels. The five largest US growth companies (all of which are part of the Magnificent 7 referred to above) reported generating $139.5 billion of cash from operations in Q4 of 2023. With around two thirds of companies having reported, US company earnings are solidly beating expectations and analysts are lifting earnings forecasts in response.

Despite our enthusiasm for US equities in the long term, it is worth noting that owing to the rise in share prices outpacing the rise in corporate earnings, US equities are now trading at an historically high level, at close to 21 times forward earnings. Given that earnings growth and the likely downward trajectory of inflation and interest rates are not guaranteed, we must try to assess whether the market is correctly valuing the potential for growth versus the risks. The Bank of America bull and bear indicator rose to 6.8 in the first week of February, a reading above 8 typically indicates the bullish trend has run too far.

Is inflation sticking

Market sentiment briefly flipped like a pancake on Shrove Tuesday as the US Consumer Price Index (“CPI”) came in at 3.1% year-on-year versus 2.9% expected and US Treasuries and equities sold-off on the news. The news disrupted a series of data pointing to falling inflation and economic growth that had helped drive the share price of large US companies up over 25% in 12 months. Investors had been expecting the Federal Reserve (“Fed”) to start cutting rates, with many arguing that the Fed was taking too long to get started, but the CPI news saw the probability of a cut in March fall substantially. The inflation figures reflected increases in the price of food, car insurance and medical care. The largest contributor was shelter costs, which surprisingly increased 0.6% in January. The CPI’s shelter component includes rent and homeowner’s equivalent rent. Economists see a moderation in this area as key to bringing inflation down to the 2% target. Equities rebounded fairly strongly after the initial reaction of markets on Tuesday, with prices reversing much of their losses by the end of Wednesday.

Regional US banks

Fears about the health of smaller US banks has risen again a year after the collapse of Silicon Valley Bank triggered a regional banking crisis. Regional bank bonds are under pressure because of their exposure to the commercial real estate market and the risk that higher interest rates will lead to an increase in defaults. New York Community Bancorp (“NYCB”) has been attempting to reassure investors about its deposits, liquidity and governance following its recent earnings release which sparked a dive of c.60% in its shares and a decision by Moody’s to cut the bank’s long-term debt rating from Baa3 to Ba2, a level at which the bonds are considered speculative. The turbulence with NYCB dragged down the value of other regional banks, with the Keefe, Bruyette, and Woods (“KBW”) Regional Bank Index seeing all 47 members losing ground, as concerns grow over the industry’s vulnerability to a high interest rate environment.

Oil M&A is hot

Diamondback Energy Inc has agreed to buy Endeavor Energy Resources LP, a fellow Texas oil and gas producer, in a deal that will produce the largest operator focused on the Permian Basin worth more than $50 billion. The latest acquisition comes following three major mergers during the last four months in US shale oil, all worth over $10 billion. This comes at a time of high demand for oil, despite efforts to transition away. Oil prices rose in the second week of February as OPEC maintained their forecast of strong demand in 2024. The group expects world demand to rise by 2.25 million barrels a day in 2024.

Economic Updates

The final January composite Purchasing Managers Index (“PMI”) for the Euro area was 47.9, whilst in the UK there was an upgrade to 52.9 vs 52.5 expected… although the UK is not in a strong position, as reflected by the announcement that the economy technically fell into recession in the final quarter of 2023 when GDP fell 0.3% having also fallen in the previous quarter. US economic growth continues to outperform European growth although the PMI index was slightly weaker than expected at 52.5.

We saw fresh signs of deflation in China, with year-on-year CPI -0.8%, the fastest decline since 2009. US CPI came in at 3.1% 0.2% higher than expected and sent 10 year Treasury yields up 13.5bps and effectively led to the market pricing in the prospect of one fewer 0.25% interest rate cut this year. UK CPI rose 4.0% year on year vs 4.1% expected.

Download the bulletin here.