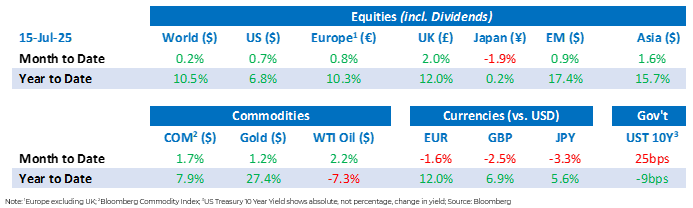

Tactical Positioning

Equity and bond markets have held steady over the last two weeks despite the ongoing tariff saga and a slight uptick in inflationary data. From here we are holding off committing new money to equity markets, for the time being, but continue to like short-dated bonds. As we wrote at the end of June, markets are due a ‘breather’ and this may extend into August but the outlook thereafter remains broadly positive supported by both high levels of investor liquidity and the return of a ‘buy the dip’ mentality.

Market Moves

On-again, off-again

Tariff and trade policy chatter dominated headlines over the fortnight with President Trump threatening US trading partners with new import taxes on a seemingly daily basis. The 90-day reciprocal tariff deadline on 9th July was replaced with a new, 1st August cut-off, with “no extensions granted” and whilst early trade deals with the likes of Vietnam were struck, many nations were left scrambling after receiving ‘trade letters’ with proposed tariffs coming into effect from the new deadline.

At the time of writing, Trump’s proposed plans are to implement 30% tariffs on European and Mexican goods, 35% duty on Canadian goods, a hefty 50% tariff on Brazilian products and 100% secondary tariffs on Russia unless a ceasefire deal in Ukraine is reached within 50 days. The sweeping tariffs have raised nearly $64bn in extra customs revenue for the US in Q2 2025, but investors will be hoping that the widely used acronym of “TACO” (Trump Always Chickens Out) continues to hold true. Despite the uncertainty, equity markets showed their continued resilience from trade noise, with US, UK and German indices breaching new all-time highs. The price of brent crude oil fell to $68/barrel over proposed sanctions in Russia.

Tears and turmoil

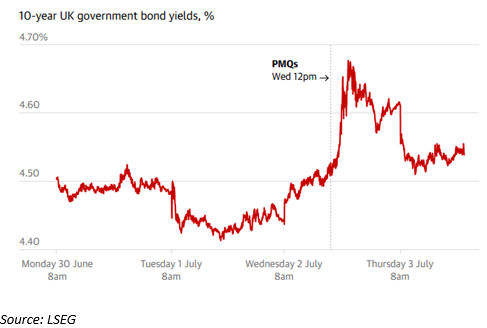

The UK bond market was plunged into disarray after Chancellor of the Exchequer Rachel Reeves appeared visibly distressed during Prime Minister’s Questions in the House of Commons, prompting fears that her political career could be nearing a premature conclusion. The yield on the 10-year gilt jumped 15.8bps to 4.61% on the day, marking the biggest sell-off since April, and, at one point, the largest single-day increase since Prime Minister Liz Truss’s mini-budget back in October 2022, as investors showed concerns that a new Labour Chancellor might adopt a more relaxed approach to fiscal policy (bond prices move inversely to yields). Sterling slumped by 1% against the dollar on the news, ending its strong run against a weaker US currency, whilst domestic-focussed UK equities fell strongly. Prime Minister Sir Keir Starmer was forced to reassure markets by claiming Reeves would be around for “many years to come”, helping reverse the daily losses seen in the UK’s currency and bond markets. News that the UK economy unexpectedly contracted by 0.1% in May, following a 0.3% fall in April, will undoubtedly come as an unwelcome blow for a Chancellor struggling to reignite economic growth in the UK.

Records are made to be broken

AI powerhouse NVIDIA saw its market capitalisation breach an historic $4trn valuation in July, shrugging off concerns around Trump’s ever-escalating trade war and competitor pressure from China. The US chipmaker has continued to prove itself as the undisputed leader behind the AI boom and the darling of Wall Street has seen its share price increase by 27% so far in 2025, having finished 2024 up 171%.

A Beautifully Big Bill

After hours of stalemate, President Trump’s controversial tax bill muscled its way through Congress by the narrowest of margins. Vice President JD Vance’s tie-breaking vote following a 50-50 split in the Senate, and a 218-214 vote in the House of Representatives helped the bill successfully pass through both chambers. The tax and spending legislation will hit the healthcare and energy sectors particularly hard, with $1trn of Medicaid cuts stripping nearly 17 million people of their health insurance coverage and forcing the closure of many rural hospitals and health clinics. The bill also expands oil and gas leasing, imposes limits on clean energy subsidies and eliminates tax credits that had lowered the cost of wind, solar and other renewable power for manufacturers and consumers alike. One major winner, however, is the $13 trillion private capital industry which celebrated lawmakers leaving the lucrative carried interest tax loophole intact, something Trump had previously pledged to eliminate. Despite the bill’s inclusion of a $5 trillion debt ceiling increase and the Congressional Budget Office’s projection that it could add an estimated $3.4 trillion to the US national debt over the next decade, markets took the eye-watering figures in their stride with US equities closing higher ahead of the Independence Day holiday.

Crypto week

The price of bitcoin hit a record high on 14th July, surpassing $123,000 for the first time as US lawmakers prepared to consider legislation aimed at making America the world’s “crypto capital”. The House of Representatives are to vote on three new acts this week, designed to create a legal federal framework governing the likes of stablecoins, putting in place regulation of cryptocurrencies and allowing the Federal Reserve (“Fed”) to create its own digital currency. Bitcoin has moved up 75% since the election in the US last November.

Economic Updates

With Donald Trump mounting renewed pressure on the Fed to lower interest rates, the unexpected increase in the May Job Openings and Labor Turnover Survey certainly poured cold water on the prospect of any monetary policy loosening. The report signalled a tighter labour market in the US. Job openings, which are a key component of labour demand, moved up 374,000 to 7.76 million, far exceeding the projected 7.32 million and marking a six-month high.

The Q2 corporate earnings season kicked off with several large banks and asset managers leading the way. Analysts have cut their US second quarter earnings growth expectations from around 9% to 5%, mainly owing to tariff fears, but the big banks JP Morgan, Wells Fargo and Citibank reported upbeat earnings and Goldman Sachs profits jumped 22% thanks to a record period from their investment banking division.

Download the bulletin here.