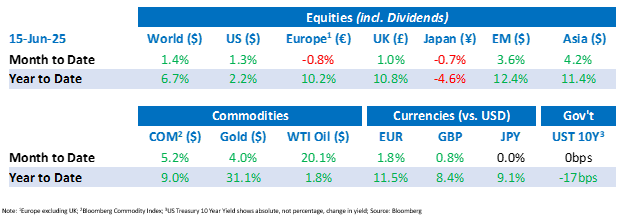

Tactical Positioning

With a new outbreak of military conflict in the Middle East, investors are weighing up the risk of regional contagion. History suggests that this will pass but the risk of the US being dragged into a conflict is never too far away. After a strong showing for markets in May, June has been more subdued, notwithstanding some volatility in the last few days. The news on inflation has generally been good and the tariff ‘war’ seems to have become less impactful as trade negotiators get around the table and the Trump camp gives more time for discussions to be concluded. Markets now await the Federal Reserve’s decision on US interest rates (18th June) and an update on US corporate results to be released in July. If the Israel/ Iran conflict is contained, we expect equity and bond markets to consolidate around current levels.

Market Moves

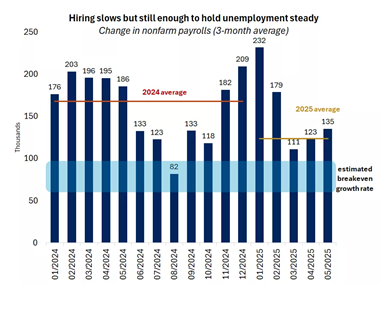

The labour market remains resilient

The latest US jobs report for May 2025 highlights the continued resilience of the US labour market despite a slight slowdown in job growth. The economy added 139,000 jobs in May, bringing the three-month average increase to 135,000 a month. Unemployment remains steady at 4.2%, signaling a somewhat robust labour market despite recent economic uncertainty around tariffs. Against this positive view, there are signs of weakness on the horizon as continuing jobless claims have reached a recent high and the Conference Board’s job availability sentiment indicator (“the labour differential”) has reached one of its lowest points over the last 12 months.

Markets reacted to the jobs data sending equities higher and bond prices lower: the labour market feels strong enough to support the economy and delay the Federal Reserve (“FED”) from cutting interest rates. Given the risk of tariff induced inflation and steady employment, the FED is likely to maintain its “wait and see” stance on interest rates having held rates steady since December. While challenges like policy uncertainty loom, the labour market’s resilience provides a stable foundation for market sentiment in the near term.

ECB cuts rates again

On 5th June, the European Central Bank (“ECB”) cut its three key interest rates by 25 basis points, lowering the deposit facility rate to 2%, the main refinancing rate to 2.15% and the marginal lending facility to 2.4% and signals a shift in tone as core euro-area growth weakens and inflation settles near the 2% long term target. Markets reacted positively with bond prices rising and equities rallying on hopes that lower borrowing costs would support corporate earnings and consumer demand. The euro fell against the dollar on the day given the widening in the difference between interest rates in the US and Europe. However, the euro is still 11.5% higher against the dollar this year. The ECB’s messaging remains the same, stressing the governing council must continue to monitor the data on a meeting-by-meeting basis allowing the flexibility to pivot in case of unexpected inflation or a growth shock.

This is in direct contrast to the FED, which is expected to hold rates steady at the meeting this week.

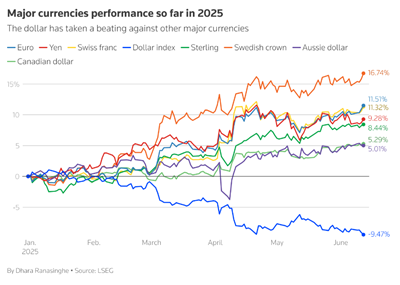

Dollar nosedive?

The dollar has lost almost 10% so far in 2025, hitting its weakest point since April 2022. This decline reflects investor expectations of upcoming FED rate cuts, the recent US-China trade softening, the move in capital away from US assets and concerns relating to the extent of US indebtedness. Scandinavian currencies have been the best performing currencies this year, advancing around 12-14%.

A softer dollar is a double-edged sword for markets. On one side, it reduces the cost of commodity prices and supports US multi-national corporations’ foreign earnings. On the other hand, it has stirred inflation worries owing to higher import costs amongst tariff trade uncertainty.

For corporate treasurers and global investors, the move repriced currency hedges and has sparked interest in non US bonds.

Trade war progress?

On 5th June, a phone call between US President Trump and Chinese President Xi yielded progress in trade discussions, particularly regarding tariffs and critical minerals. This development alleviated some market concerns about escalating trade tensions, following a tumultuous April when Trump introduced his policy on tariffs. Following the meeting, US equity markets rallied, particularly the technology and consumer discretionary sectors. Chinese equity markets also advanced, rising 0.9% and the Hong Kong market up 2.2%. The Chinese yuan strengthened marginally against the US dollar. However, markets remain cautious as finalised agreements are not yet in sight and tariff-related uncertainties persist.

Geopolitical tensions rising again…

Israeli forces struck Iranian military and nuclear facilities on the last day of the fortnight intensifying the already high Middle Eastern tensions. The escalation, coupled with US President Trump’s call for Iran to agree to a nuclear deal, heightened investor caution causing significant market volatility among commodities and some sectors. In response to the attack and Iran’s subsequent reaction the oil prices surged approximately 8%, its largest one-day spike since March 2022; safe haven assets, including gold and US Treasuries also climbed higher with the US 10 year yield briefly dipping below 4%. The US equity market fell on Friday by over 2% initially in response to the news before recovering part of the fall.

Economic Updates

In the US, the Consumer Price Index (“CPI”) rose to 2.4% from 2.3% previously. US crude oil inventories fell by around 3.6m barrels in the first week of the month and are about 8% below the average level of the past five years. In the UK, month-on-month GDP contracted 0.3%, markedly below expectations following an increase of 0.2% last month. In Asia, the Caixin manufacturing PMI’s decline to 48.3 in May demonstrated the impact of US tariffs on Chinese exporters. A reading below 50 indicates falling demand.

Download the bulletin here.