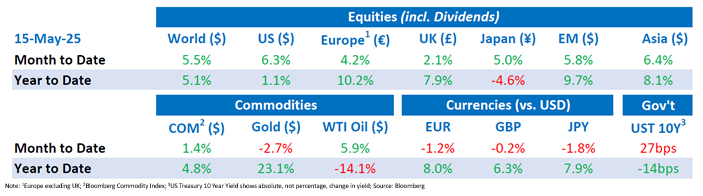

Tactical Positioning

Following the equity market rally of the last two weeks, which we discuss below, it might be time for a pause. Although investor sentiment has become distinctly more positive it may be too early to assume that the tariff ‘battle’ has been won and there is blue sky ahead. In the short-term markets have received a reminder that US spending and the growing deficit might be a drag on the US economy with the credit agency, Moody’s, cutting its US credit rating and pointing out that interest payments on US debt could consume up to 30% of government revenues in the next 10 years. Whilst investors may shake off this worry as the US continues to prosper, it has created an inflection point for bond markets and this may feed into equity markets over the coming days. Overall, we remain positive on equities and shorter dated bonds but are reluctant to chase markets after such a solid recovery in a relatively short period.

Market Moves

Equity market recovery continues

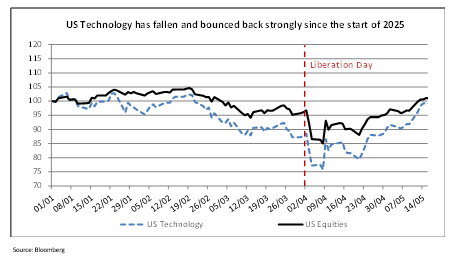

Equity markets had a strong fortnight led by growth-oriented sectors. Technology and consumer discretionary stocks have each climbed more than 20% since the April lows, while small- and mid-cap equities have posted gains of over 19%. Meanwhile, defensive sectors such as consumer staples and healthcare, which led during the downturn, have trailed in the rebound. Market breadth has improved and volatility has declined, although sentiment remains sensitive to further policy shifts.

UK equities were a notable underperformer during the fortnight, with the market up just 2.1% versus 5.5% for global markets. Performance was held back by the indices’ heavy exposure to commodities and financials, alongside subdued domestic economic momentum.

Tariffs, tech, and turnarounds

On 8th May, President Donald Trump announced a bilateral trade agreement with the United Kingdom, marking the first deal struck with a major trading partner since the sweeping tariff measures introduced on “Liberation Day” (2nd April). The US-UK agreement rolls back punitive levies on British steel and car exports but keeps the universal 10% US levies on most UK exports. From a global economic perspective, the deal is symbolically significant but limited in impact: the UK accounts for just 2% of US goods imports and 4% of US exports. Broader tariffs on major trading partners remain in place, leaving the overall trade environment fragile. After falling 19% between 19th February and 8th April, the US market has recovered to near flat on the year (as shown in the chart below). The rebound has been driven by a marked de-escalation in US-China tensions, culminating in a 90-day tariff truce announced on 12th May. The US reduced tariffs on most Chinese imports to 30% from 145%, while China reciprocated with cuts to 10% from 125%.

Although the agreement has effectively ended a short-lived trade embargo, analysts warn that the longer-term structural effects, particularly supply chain realignment, will take time to unwind. Even so, the agreement has gone a long way to restoring investor confidence. The return of confidence has also been reinforced by a growing belief that, despite his combative rhetoric, President Trump consistently softens tariff threats in response to market pushback. While risks remain, investors are increasingly pricing in the likelihood of more moderation than escalation.

Petro politics: Gulf capital comes to America

During his visit to Saudi Arabia on 9th May, President Trump announced a $600 billion investment commitment from the Kingdom into US industries, spanning defense, energy, infrastructure, and advanced technology. The package includes a record $142 billion arms deal, which is supportive for US defence contractors, and $20 billion from Saudi company DataVolt into US data centres and energy infrastructure. US tech firms including Google, Oracle, Salesforce, and AMD also pledged over $80 billion in reciprocal investment across both countries. The timing is significant: the deal was unveiled just days amid heightened scrutiny of OPEC’s role in recent oil price volatility. While the agreement will likely be rolled out over several years, it signals a potential reorientation of Gulf state capital flows toward long-term strategic assets across a range of sectors. Investors may view this as a supportive signal for US industrial policy and a partial hedge against future geopolitical disruptions in energy markets.

Warren Buffett – buy low, be patient and retire high

Warren Buffett has announced that he is stepping down as the CEO of Berkshire Hathaway at the end of this year, ending a six-decade run at the helm of one of the world’s most closely watched investment vehicles. While he will remain as chairman, day-to-day leadership passes to Greg Abel, long flagged as his successor. Berkshire shares fell 5%, as markets absorbed the transition from Buffett’s stewardship to a more institutional model. Abel inherits a $300 billion equity portfolio and a reputation to uphold. While the transition was well-telegraphed, Buffett’s exit marks the end of an era and a subtle recalibration in how investors may view Berkshire going forward.

Economic Updates

US inflation for April as measured by the Consumer Prices Index was modestly behind the expected 0.3% at 0.2% bringing the annual rate to 2.3%. The April non-farm payrolls report revealed a stronger than expected increase of 177,000 jobs, while the US unemployment rate held steady at 4.2% highlighting ongoing labour market strength in the US.

The Philadelphia Fed Manufacturing Index delivered a much better than expected reading of -4.0 compared to an expected -11.3 and previous -26.4. This may reflect a stronger than expected economy.

In terms of monetary policy, the Federal Reserve kept interest rates at 4.5%. In the UK, the Bank of England delivered its fourth consecutive rate cut, lowering the base rate to 4.25%, but a rare three-way split on the Monetary Policy Committee surprised markets and cast doubt on the pace of further easing. While two members pushed for a larger cut, citing global trade risks, others, including Chief Economist Huw Pill, voted for no change, warning that wage growth and sticky services inflation remain a threat.

Download the bulletin here.