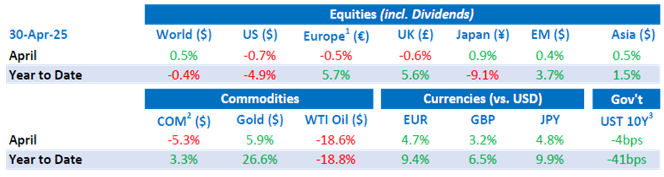

Tactical Positioning

Market Moves

Boom

Trump promised a boom in his first 100 days in office, reached on the 30th April. The reality of the ‘boom’ largely depends on how one chooses to define it. The stock market has been marked by volatility and despite last week’s rally, the index of leading US companies is down 8% since the President’s inauguration. Traders had gone ‘all in’ on the administration, which saw US equities posting their best post-election gain ever. However, the disruption of tariffs, combined with other policy uncertainty such as removing illegal immigrants and the firing of federal employees has unnerved investors. Expectations of volatility in stocks, bonds and currencies are all higher than 100 days ago. Words out of the White House on the 100th day of this administration by Trump on Truth Social were “When the boom begins, it will be like no other. BE PATIENT”. The US economy fell 0.3% over the first quarter vs expected growth of 0.4%. However, this number was distorted by a large increase in imports, ahead of the tariff announcements and it is not necessarily a reflection of any longer-term trend.

An independent central bank?

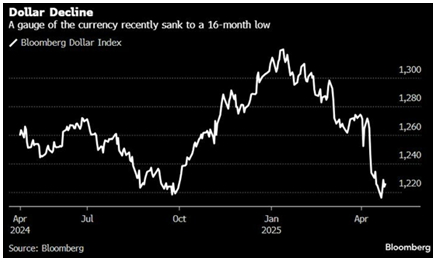

President Donald Trump has been increasingly critical of the Federal Reserve (the Fed) and in particular its chair, Jerome Powell. Trump posted on Truth Social that the Fed had been too slow to cut interest rates, that there was “Virtually No Inflation” and that “Powell’s termination cannot come fast enough!”. As investors concerns grew regarding the safety of US central bank independence, US Treasuries sold off. The yield of the 10-Year note rose above 4.4% and the 30-Year yield rose to 4.9% before Trump stated that that he had ‘no intention of firing’ Powell. The back and forth, coupled with concern around the potential inflationary impact of the proposed tariffs, is impacting not only the traditional safe haven of US Treasuries, but also the US Dollar, which measured against a basket of major currencies is on track for its steepest monthly decline since the Global Financial Crisis of 2007-09 (down around 9% this year). This has been amongst a broader loss of faith in American assets as investors focus on potential economic damage. As investors battle the President’s unpredictability, other safe haven assets have been well bid (Japanese yen +6.7% in April) and in particular gold, which reached a new intraday high of $3,500. Goldbugs in China have been busy over the last few weeks with the country responsible for $7.4bn of inflows into gold exchange traded funds in April.

Elbows Up

Mark Carney’s Liberal Party won the Canadian election on Tuesday by a narrow margin. The election results mark a turnaround for the party which was predicted to lose four months ago. The Canadian dollar initially rose after victory was called for the Liberals but this reversed as it became clear the vote was close – indicating potential government instability. The former Bank of England Governor campaigned on strengthening Canada’s economic independence as the country navigates its response to Trump. Canada is one of the most exposed countries to a trade war about three quarters of its exports go to the US including the vast majority of its oil and gas exports. Carney’s acceptance speech was notable in its thanks to Donald Trump for his victory and in its description of the US tariffs policy as “stupid.”

Chocoholics

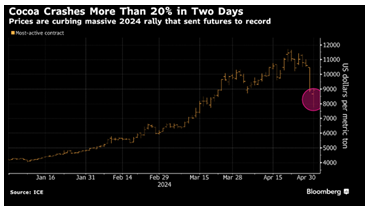

Cocoa has been bouncier than an Easter Bunny. In 2024, prices nearly tripled, reaching an all-time high of $12,391 per tonne in December 2024, but this year they have fallen by over 30% to below $8,000 per tonne. The decline is attributed to improved weather conditions in West Africa and increased production forecasts. This week, futures prices in New York experienced an historic crash at one point falling by 27%, the biggest two-day decline going back to 1960. The Trump administration announced tariffs of 21%, the highest in West Africa, on the Ivory Coast (the world’s largest cocoa producer) which after the 90 day pause have the potential to drive the cost of cocoa higher and destabilise the market. A strong stomach has been required for those who may have been tempted to overconsume recently!

Economic Updates

In the last two weeks of April, data out of the UK saw headline inflation falling to 2.6% (vs 2.7% expected), whilst core CPI was in line with expectations at 3.4%. UK house prices fell 0.6% month on month in April, below the zero growth forecast by economists

April flash Purchasing Managers Indices (“PMI”) readings from around the world offered an initial indication of the global economy’s reaction to tariffs. The US composite PMI was 51.2, its weakest print since December 2022. The Euro Area composite PMI was 50.1, remaining just inside expansionary territory. In the UK the composite PMI was 48.2 against a forecast of 50.5. The Conference Board consumer confidence indicator fell to 86.0 in April (vs. 88.0 expected), the weakest since May 2020.

US inflation as measured by Personal Consumption Expenditure edged lower to 2.3% p.a. in March from 2.5% in February, the US Bureau of Economic Analysis reported on Wednesday. This reading came in above the market expectation of 2.2%.

Download the bulletin here.