Tactical Positioning

In our review, we cover some of the key features that have helped propel markets forward in the last two weeks. It seems to be the case that staying relatively fully invested in equities and bonds has been the best strategy over the last few months despite a high degree of ‘policy chaos’ and the uncertainties brought on by geopolitical events. Interestingly, most stock market historians will point out that sell-offs induced by policy confusion or global geopolitics are often good buying opportunities with quick recoveries and solid medium-term gains. Whilst markets are due a ‘breather’ we suspect there could be further progress across the year helped by falling interest rates and a potential boost from spending in Europe and lower taxes in the US. At present the spectre of a damaging trade war seems to be evaporating too.

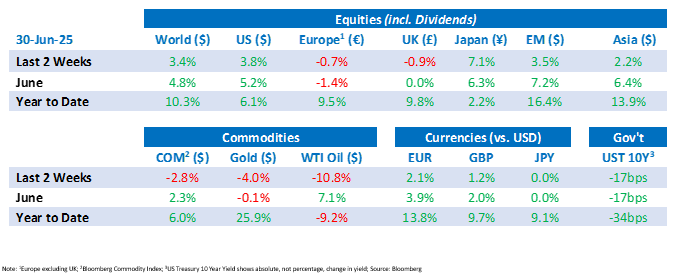

Market Moves

Wall Street’s winning streak continues

The US stock market surged to new heights at the end of June 2025, rebounding from the ‘liberation day’ induced slump in April. The rally has been fuelled by a combination of geopolitical easing, particularly a finalised trade framework between the US and China and optimism surrounding potential deals with other major partners, robust corporate earnings, highlighted by Nike’s 15% climb, and expectations of a US$4.5 trillion tax cut bill advancing through Congress. Investor confidence was further bolstered by strong performances in technology and AI-related stocks, with companies like NVIDIA and Microsoft leading the charge. Despite a brief dip following President Trump’s announcement to halt trade talks with Canada over its digital services tax, which was subsequently dropped by Canada, markets quickly regained momentum. The market’s ability to shake off volatility and push to new records underscores a broader sentiment: investors seem to believe that the worst of the year’s turbulence may be behind them.

Oil’s volatile ride in June

Oil prices tumbled in late June as geopolitical tensions in the Middle East cooled and expectations of increased oil supply began to weigh on markets. Following a ceasefire between Israel and Iran, Brent crude dropped to around US$67 per barrel, down from highs of around US$80 earlier in the month. The 12-day conflict, which had sparked fears of a disruption in oil flows through the Strait of Hormuz, initially sent prices soaring. Earlier tensions were also intensified by a US air campaign on 22nd June which targeted Iran’s key nuclear sites. President Trump hailed the strikes as a decisive blow to Iran’s enrichment program, though the head of the United Nation’s nuclear watchdog concluded the damage was ‘severe’ but not ‘total’. Iran’s measured retaliation, a missile barrage on the US Al-Udeid base in Qatar that caused no casualties, signalled its intent to avoid escalation, easing market fears. In parallel, the energy market digested signals of rising supply. OPEC+ is expected to boost production by 411,000 barrels per day in August, marking a steady unwind of prior output cuts. Domestically, the US administration pushed for energy expansion, with Trump publicly urging producers to “DRILL, BABY, DRILL.” While market sentiment has stabilised for now, the situation remains fragile, particularly around the Strait of Hormuz, a chokepoint for nearly 20% of global oil shipments.

US renewables continue to face headwinds

A sweeping Senate bill backed by President Trump and labelled by Elon Musk as ‘utterly insane and destructive’ has sent shockwaves through the clean energy sector by proposing the immediate rollback of key tax credits for wind and solar projects and introducing a new tax on those completed after 2027. The legislation would end incentives established under the Inflation Reduction Act, replacing them with stricter eligibility rules and penalties for projects using components from China. Clean energy industry leaders warn the bill could derail hundreds of billions in investments, raise electricity costs, and jeopardise US leadership in renewable energy. Critics also argue it favours fossil fuels and undermines climate progress.

Rediscovery of emerging markets

Emerging market assets have rallied in 2025, outperforming developed markets despite US trade tensions and instability in the Middle East. Emerging market equities have risen by nearly 16% year-to-date, almost twice the return of developed market equities, as investors return to undervalued local currency assets, drawn by high inflation-adjusted yields and a weaker US dollar. The shift is driven by concerns over US policy uncertainty which is leading investors to diversify their equity portfolios more broadly, growing confidence in countries such as China and Brazil and structural appeal in sectors including technology. Modest capital inflows have also fuelled strong performance, marking a significant rebound after years of underinvestment.

Economic Updates

In the US, the Federal Reserve’s (“FED”) primary inflation gauge, the personal consumption expenditures price index (“PCE”), increased by 0.1% over the month, resulting in an annual rate of 2.3%. Excluding food and energy, core PCE rose 0.2% over the month, resulting in an annual rate of 2.7% which was 0.1% higher than estimated. In the UK, CPI inflation fell to 3.4% in May, down from the previous month’s reading of 3.5% and in Canada, annual CPI inflation rose 1.7% in May, in line with expectations.

GDP data released in June showed the US economy contracted 0.5% in the first quarter of 2025, lower than the 0.2% contraction forecast. In the UK, GDP grew by 0.7% in the first quarter, in line with the estimate. In Canada the latest GDP release showed a 0.1% decline over the month of April, lower than the 0.0% forecast.

Central bank meetings took place in the second half of June with the Bank of England maintaining its policy rate at 4.25% and the FED leaving its rate unchanged at the 4.25% – 4.50% range. The Bank of Japan also kept its policy rate at 0.5% while the Swiss National Bank reduced interest rates by 25 basis points to zero.

Download the bulletin here.