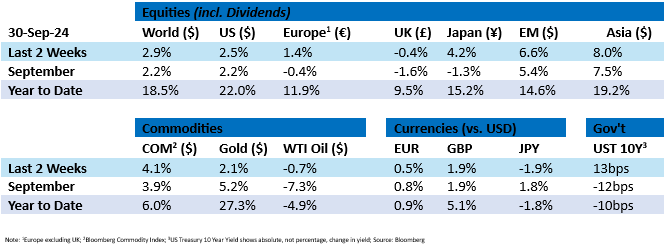

Tactical Positioning

Equity markets finished September with a flourish, but we are left gazing at a complicated situation in the Middle East. The oil price is often seen as a barometer of tension in the region and so far it has remained remarkably subdued showing a drop of over 15% in the last 3 months, partly helped by Saudi Arabia’s decision to increase production. However, with many equity indices standing at all-time highs, markets may find it difficult to maintain their positive momentum as investors can be wary of increasing geo-political tensions. Whilst we are comfortable with our full weighting in bonds and equities, day-to-day movements in markets could be erratic. As we move further into October, the US Q3 results season will start (around 11th Oct) and we may see another interest rate cut in Europe. The US and UK will be considering their own interest rate policy in early November. Given that the world seems more comfortable that inflation has normalised we have diversified our bond exposure by taking on some longer maturity bonds, thus locking-in to what may turn out to be attractive rates if interest rates continue to fall, as currently expected.

Market Moves

The Fed cuts interest rates

The Federal Reserve (“Fed”) cut interest rates by 50 basis points on 16th September, the first rate cut since March 2020 and a response to inflation moving closer to the Fed’s 2% target. Equities initially reacted well and long-term US Treasury yields fell reflecting expectations of lower interest rates. However, concerns about the outlook for inflation and the timing of further cuts led to bond yields later reversing course. US stocks ended September at record highs, performing much better than is normal for the month – since 1928 September has on average been the worst-performing month of the year. The US dollar weakened against the euro but strengthened against the Japanese yen. More recently, Fed Chair Jerome Powell stated at the National Association for Business Economics that there is no “hurry” to cut rates, acknowledging that the US economy is in “solid shape” and that 25 basis point rate cuts are expected in November and December. Investors are expecting larger cuts with markets pricing in rates being lowered by 75 basis points by the end of the year.

China’s Economic Recharge

In a bid to boost the economy, China announced plans to lower borrowing costs and allow banks to increase their lending. The People’s Bank of China has committed to cutting the reserve requirement ratio – the amount of cash that banks must hold as reserves – by 50 basis points and to cutting a key policy rate by 0.2% to 1.5%. These measures will provide liquidity and encourage borrowing. China’s property sector in particular has been struggling so an interest rate cut of 0.5% on existing mortgages is being introduced and the minimum down payment on property will decrease to 15%. In the week following these announcements, Chinese stocks rallied and achieved their highest daily gain since 2008 on 30th September.

US strikes

US East Coast and Gulf port workers have gone on strike after the contract between the International Longshoremen’s Association and the United States Maritime Alliance expired on 30th September. President Joe Biden has the power to suspend the strike for 80 days under the federal Taft-Hartley Act but has resolved not to. Although imports over the summer increased to mitigate the impact of this impending strike, time sensitive imports are likely to be impacted in addition to retail goods and other products. More than 10,000 workers may be on strike and more than a third of imports and exports may be affected. This could cost the US economy approximately $4.5 billion a week whilst the strike continues. Ahead of the November election the Democrats will have to consider the risk of alienating their allies in the labour movement by stopping the strike and easing the inconvenience of delays. Depending on the length of the strike, it could be inflationary and put jobs at risk.

A crude awakening

It was reported over the fortnight that Saudi Arabia is willing to abandon its unofficial price target of $100/barrel for crude oil and is preparing to increase output. Unlike other Organisation of the Petroleum Exporting Countries (“OPEC”) such as Iraq and Kazakhstan who have been pumping above their quotas, Saudi Arabia has been voluntarily producing below its maximum capacity. This decision to increase output may merely be a warning to other members to pump what has been agreed. However, if Saudi Arabia follow through, this will be welcomed by those countries that benefit from lower fuel prices. Production cuts amongst the OPEC members were due to be reversed from the start of October: however, there has been a two month delay from other members.

Economic Updates

In the US, the Fed’s preferred inflation indicator, the Core Personal Consumption Expenditures Price Index, which excludes food and energy rose 0.1% in August and was up 2.7% from a year ago.

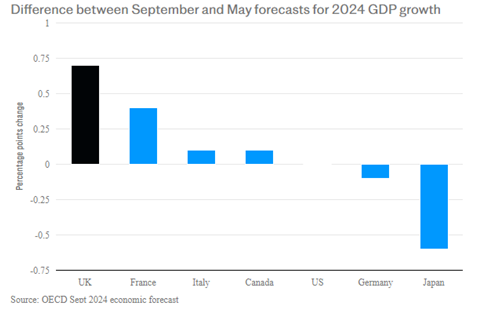

According to the UK’s Office of National Statistics, public sector net debt in the UK, excluding public sector-owned banks, rose to 100% of Gross Domestic Product (“GDP”) in September for the first time since monthly records began in 1993. UK government debt was last at this level on a regular basis when the UK was still coping with the financial repercussions of World War Two in the early 1960s. Conversely, in positive news for the UK, the Organisation for Economic Cooperation and Development has upgraded its forecast for 2024 UK GDP growth by the most of all countries in the G7, increasing their prediction by 0.4% to 1.1%. 1.2% growth is estimated for 2025. Germany’s projection was cut from 0.2% to 0.1% for 2024 and Japan’s fell from 0.5% to -0.1%. Canada and France’s growth is forecast to increase to 1.1% too. The US leads the pack with GDP growth expected to be 2.6% this year.

Furthermore, in the period, sterling reached a two-year high against the euro. In Europe the leading Global Composite Purchasing Managers’ Index for the euro zone reduced to 48.9 in September from August’s 51.0 (any number below 50 reflects an anticipated contraction in demand), with Germany’s decline worsening and France returning to contraction following a boost in August due to the Olympic Games. In the UK the index also fell in September although at 52.9 it remains comfortably above 50.

Download the bulletin here.