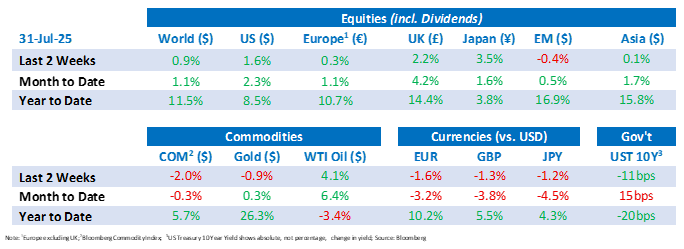

Tactical Positioning

The end of July has brought with it new all-time highs for several equity indices. However, it has been a narrow rally led mainly by technology stocks. As we wrote in our last Bulletin, investors need a ‘breather’ to understand the impact of the tariff changes imposed by President Trump. Although the world can live with average US tariffs of around 15% it is a huge increase on the previous average US tariff on overseas exporters of just 2.5%. With lower equity and bond trading volumes likely over August and most central banks in recess, there is a reasonable chance that investors might start to bank some profit with a view to reassessing the situation in September. For now, we continue to hold off committing new money to equities.

Market Moves

Trump vs. Powell

The Federal Reserve (“Fed”) kept its benchmark rate unchanged for the fifth straight meeting, publicly defying President Trump’s repeated calls for cuts to spur borrowing and boost housing. The Committee voted 9-2 to hold rates between 4.25% and 4.50%, as governors Michelle Bowman and Christopher Waller cast dissenting votes, the first double dissent by Fed board members since 1993. The majority opted to await clearer signals from inflation and employment data before adjusting policy at the September meeting. Chair Jerome Powell emphasised the bank’s independence and data-driven mandate, brushing off political pressure by highlighting persistent inflationary pressures and a robust labour market that argue against easing. Trump responded with a scathing social media barrage, branding Chair Jerome Powell “Too Late,” “TOO ANGRY, TOO STUPID, & TOO POLITICAL”, accusing him of costing the country trillions and overseeing an “incompetent, or corrupt, renovation” of the Fed’s headquarters, while demanding immediate rate cuts.

Deal with it

The United States and the European Union have struck a landmark trade deal that sets a 15% flat tariff on 70% of EU goods entering the US, half the 30% levy President Trump threatened, and maintains 50% duties on steel and aluminium. In exchange, the EU commits to purchasing US$750 billion in US energy products over three years and making US$600 billion in new investments in the US. The EU has also agreed to eliminate duties on US industrial exports into the EU as well as provide better access to the EU market for US fishery products and non-sensitive agriculture exports. In addition, zero-for-zero tariffs have been established on strategic goods, covering aircraft and their components, selected chemicals and generics, semiconductor equipment, specific agricultural products, natural resources and critical raw materials.

Elsewhere, Britain and India have signed a free trade agreement, Britain’s largest since Brexit, that will cut or eliminate Indian tariffs on 90% of UK imports, bringing the average to 3% from 15%. The changes include a reduction in duties on UK whisky and gin, initially dropping from 150% to 75% and then to 40% by the tenth year, while car tariffs will fall from over 100% to 10%. In return, the UK will grant zero duties on 99% of Indian exports. Negotiations launched in January 2022 overcame long-standing political and technical hurdles, and the pact is expected to raise UK GDP by around £4.8 billion annually.

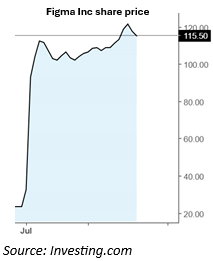

Figma blasts onto the scene

On 31st July, Figma, a software design company, priced its initial public offering (“IPO”) at US$33 a share, raising US$1.2 billion with an order book which was oversubscribed by more than forty times. On its first trading day on the New York Stock Exchange, the stock vaulted 250% to US$115.50, briefly triggering multiple trading halts and pushing its fully diluted market value above US$60 billion. The event marked the largest US venture-backed tech listing since Rivian, rewarding early backers with sizeable gains. Figma’s debut signals a revival in the IPO market and cements the company’s rise from a failed US$20 billion Adobe takeover to one of the most eagerly watched software listings of 2025.

Global climate targets falling short

A new report published by Ember, a global energy thinktank, has revealed that despite the global pledge at COP28 to triple renewable energy capacity by 2030, national commitments remain largely stagnant. As of July 2025, only 22 countries, with just seven outside the EU, have updated their 2030 targets, with most changes arising from routine planning rather than direct responses to the pledge. The global sum of national targets has increased by only 2% since COP28, reaching 7.4 terawatts (TW) which is much lower than the 11 TW needed to meet the tripling goal. Major emitters including the US, Russia and Canada have yet to revise their targets, and only a few countries, such as India and Saudi Arabia, have plans aligned with the pledge. The report highlights that without swift and ambitious national updates, the world risks missing a critical opportunity to stay on track for the 1.5°C climate pathway.

Economic Updates

In the US, the core personal consumption expenditures price index (“PCE”), increased by 0.3% over the month, resulting in an annual rate of 2.8% which was above expectations, signalling persistent inflationary pressures. Additionally, the number of weekly initial claims for state unemployment benefits increased was 218,000 to 26 July marginally below expectations.

GDP data released in July showed the US economy increased at an annual rate of 3.0% in the second quarter of 2025, primarily as a result of a decrease in imports. In Europe, GDP increased by 0.1% in the euro area and by 0.2% in the EU over the second quarter, equating to 1.4% and 1.5% over the year. Output from the EU’s largest economy, Germany, fell by 0.1% in the second quarter and rose 0.4% over the year. In Canada, the latest GDP release showed a 0.1% decline over the month May, matching the April reading.

Central bank meetings took place in the second half of July with the European Central Bank maintaining its three key interest rates unchanged, with the deposit rate facility held at 2%. In the US, the Fed kept its rate unchanged at the 4.25% – 4.50% range and in Canada, the Bank of Canada maintained its target for the overnight rate at 2.75%. The Bank of Japan also kept its policy rate at 0.5%.

Download the bulletin here.