Tactical Positioning

Geo-political events have taken centre stage in the last two weeks at a point when markets, as we mentioned in our last Bulletin, were flashing ‘overbought’. To date, the pull back has been around 3% to 5% across the main equity markets and this may be just enough to start to tempt a few ‘buy the dip’ investors to step forward. In our view, the fact that interest rates will be falling imminently in EU and probably by the end of the summer in the US and that earnings growth is unlikely to get knocked off course by geopolitical events, there is enough reason to add to equities and bonds where we hold excess cash. In addition, we are looking at quoted assets that stand on a deep discount to their asset value on the basis that the ‘normalisation’ of stock markets could have a positive effect on their prices.

Market Moves

US inflation comes in hotter than expected

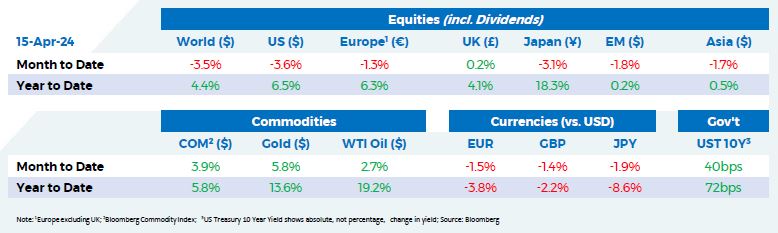

The latest US Consumer Price Index (“CPI”) data surprised on the upside with headline inflation coming in at 3.5%, marginally ahead of the 3.4% forecast with rising shelter and gasoline prices having an impact. Core CPI, which strips out food and energy costs, was also slightly above consensus at 3.8%. Momentum on the disinflation path appears to be reducing and we may need more stubborn areas of the index, such as shelter costs, to fall in order to complete the final push towards the Federal Reserve (“Fed”) target of 2%.

Market pricing points to a low likelihood of a US rate cut at the June or July Fed meetings, with September now looking the more probable starting point. This is in stark contrast to a month ago, when markets assigned a 90% probability that we would see lower interest rates by July. As time passes, the six to seven rate cuts touted at the beginning of the year are looking ever more detached from the reality that is unfolding.

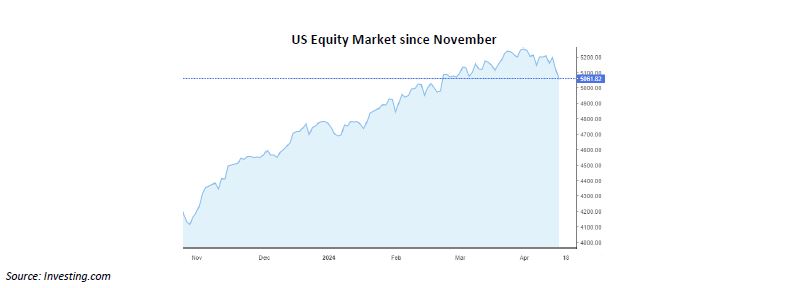

Slight pullback in leading markets

The market rally of 2024, which has seen record highs across many of the world’s leading equity indices has been momentarily stymied. This is perhaps understandable given the strength of the rally, with the US equity market experiencing nine consecutive weeks of gains. The catalyst for the reversal is the market adjusting to the new reality of fewer and later rate cuts than previously anticipated, along with the increasingly unpredictable situation in the Middle East. US 10-year Treasury yields rose to 4.63% from 4.20% at the beginning of the month, a level not seen since November last year. With the corporate earnings season now upon us, there will be hope among investors that favourable results may help propel markets forwards once again. The “Magnificent Seven” will be closely watched as always, but with Tesla announcing plans to cut 14,000 jobs, equivalent to 10% of their workforce and Apple’s iPhone sales dwindling in China, we feel that the market will become less focused on this small group of stocks.

To war or not to war?

On Saturday night, for the first time in its history, Iran engaged in direct confrontation with Israel in a retaliatory attack after the killing of key Iranian military personnel in Damascus in early April. Even though the attack was thwarted with minimal casualties by Israel and their allies (including the US, UK and France) there is undoubtedly a bigger question at play: what is next for the

Middle East and how will prime minister Benjamin Netanyahu respond? Official communication from Iran is that the ‘operation is over’ but should Israel launch a counterattack Iran would probably respond again. The oil price moved little in response – perhaps an indication that the Iranian government is to be believed, but also a reflection that the significant geopolitical risks of the region had already been priced in. That said, should things escalate further, market volatility would increase and Iran always retains the ability to cause disruption along the Strait of Hormuz, a critical trade route in the region.

Every cloud has a silver lining

One notable exception to the recent setback in prices has been silver which is up 13.8% so far this month and 19.4% this year. The recent rally in the gold price has no doubt helped silver, as investors look to protect themselves from inflation and geopolitical instability and the unique industrial characteristics of silver have generated continued demand.

Economic Updates

Euro CPI for March was 2.4%, down from 2.6% the previous month. France and Germany also released their CPI data of 2.3%and 2.2% respectively, both down from 3.0%. In their latest meeting, the European Central Bank voted to keep interest rates at 4.0%. Also in Europe, the UK is on track to exit a technical recession as GDP grew 0.1% in February, following 0.3% growth

in January. The US economy added 303,000 jobs in March, well ahead of the projected figure of 212,000. The unemployment rate also edged down to 3.8% from 3.9%.

Download the bulletin here.