Tactical Positioning

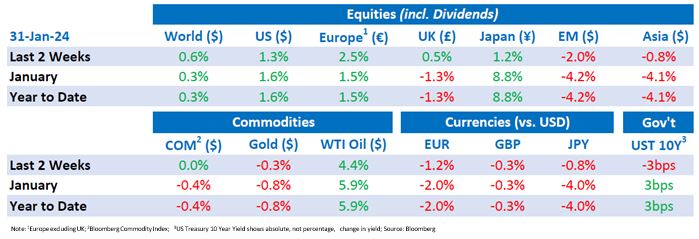

Following our Bulletin dated 15th January, there was the anticipated pause in the equity market rally, but this was very short lived and gave little opportunity for investors to add to positions. Subsequently, except for Asian and Emerging Markets which were led lower by poor numbers from China, bonds and equities resumed their upward path during the fortnight buoyed by investors’ expectations of interest rate cuts in the spring as well as decent Q4 results from several US Corporations. Our stance remains the same: maintain a full weighting in bonds and equities and those below target weightings should use setbacks and pauses to add.

Market Moves

Strength to strength

The US has begun the year from a position of considerable strength with a raft of robust economic data which helped drive the US market to a new all-time high. A significant increase in business activity was evident in both the services and manufacturing Purchasing Managers’ Indices (“PMIs”). The manufacturing PMI rose from 47.9 to 50.3 and services increased from 51.4 to 52.9: above 50 is an indicator of a growing economy. Prior to the release, both measures were forecast to stagnate or fall. The composite PMI produced the highest reading in seven months. US economic growth surprised to the upside with the latest GDP report for the fourth quarter of 2023 showing annualised growth of 3.3%, far above expectations of 2% growth. Core Personal Consumption Expenditure (“PCE”), the Federal Reserve’s (“FED”) preferred inflation measure, slowed to 2.9% year-on-year, its lowest level since 2021.

All stick, no twist

Central bankers in Europe and the US maintained their hold on interest rates at their respective policy meetings. The European Central Bank (“ECB”) held rates for the third straight meeting, with ECB President, Christine Lagarde, indicating that it was premature to discuss cutting rates and that future decisions would be based on incoming data. Despite this, the ECB’s meeting may have indicated a subtle move towards a more dovish stance with the prospect of a rate cut not entirely dismissed. This is perhaps because inflation across the eurozone is trending downwards with a slew of negative economic data. GDP data showed the bloc’s biggest economy, Germany, narrowly avoiding a technical recession in the final quarter of 2023. Markets moved to price in a quarter point cut in April and around a 1.4% total reduction in interest rates in 2024.

In the US, the FED unsurprisingly came to the same conclusion by keeping rates unchanged. Federal Reserve Chair Jerome Powell, pushed back on the prospect of any rate cuts in the coming months but suggested that inflation and employment goals are moving into better balance. The language used indicates that there are unlikely to be further rate rises in the current cycle. Whilst the prospect of rate cuts clearly provides support for equity markets, the lack of transparency from central bankers on when rates may start to fall could result in periods of fragility and ultimately present investors with some interesting buying opportunities.

Trumps and downs

Donald Trump has been ordered by a jury to pay $83.3 million in compensatory and punitive damages in a defamation case against writer E Jean Carroll. The former president is facing a growing list of criminal cases all whilst battling it out in the Republican primaries, aiming to return to the White House. Trump has become the first nonincumbent Republican ever to win both Iowa and New Hampshire contests, solidifying his position as the front runner to become the Republican presidential candidate in the 2024 election. During the 23 election years since 1937, 19 have provided positive US equity market performance with an average total return of 9.9%. This is slightly below the average return of 12.5% in years when there was not a presidential election. The average annual return in election years when the election leads to a divided government is 9.4% when a Republican president is elected and 15.9% when there is a Democratic president. In contrast the average return in years when there is a clean sweep by Republicans is 16.1% and 11.5% for the Democrats (past performance is not necessarily a guide to future performance).

China woes

China’s Evergrande has been issued with an order to liquidate from a Hong Kong court, heightening concerns facing China’s beleaguered real estate sector. Evergrande was once one of the largest property developers in China and is now one of the world’s most indebted company with debt in excess of $300 billion. Worries about the potential ripple effects from the wind up of the company were limited with the Hong Kong Stock Exchange suspending its shares. Most recent GDP data showed an uptick of 5.2% in 2023.

Economic Updates

PMI data for the Eurozone point to the bloc remaining in contraction, with the composite PMI reading at 47.9 vs an expectation of 49. Both the services and manufacturing PMI also came in below consensus expectations with the services PMI at 48.4 and manufacturing at 46.6.

Conversely in the UK, services PMI registered the highest level of expansion in eight months rising to 53.8 from 53.4 and above expectations of 53.2. Manufacturing remains in contraction at 47.3 but was above expectations and at a nine-month high. Pending home sales in the US surpassed analyst expectations, buoyed by the decline in mortgage rates. Recent reports showed an increase of 8.3% (month by month) vs. consensus expectations of 1.5%. As of 31st January, the average rate on a 30-year fixed mortgage remains just below 7%.

Download the bulletin here.